|

The Bank of Canada delivered its eighth consecutive rate hike on Wednesday, January 25, but said it would likely now pause to assess the impacts of its rate hikes to date.

As expected, the Bank of Canada raised its overnight target rate by 0.25% to 4.50%. That’s 425 basis points higher than it was this time last year.

As long as the economy performs broadly as expected, the Bank said it would "hold the policy rate at its current level while it assesses the impact of the cumulative interest rate increases.”

It added, however, that it remains "prepared to increase the policy rate further if needed to return inflation to the 2% target.”

The Bank also released its Monetary Policy Report, in which it lowered its forecasts for both inflation and economic growth.

The Bank of Canada said it expects growth to "stall” by the middle of this year—dipping to an annual rate of just 1%—before picking up towards the end of the year.

It also forecasts inflation to fall to an annual growth rate of 3.6% this year (down from a previous forecast of 4.1%), before falling to 2.3% in 2024.

"With the belief that the economy is on the path to price stability, the BoC can now step to the sidelines and let its restrictive policy filter through the economy,” noted economist James Orlando of TD Economics.

"Though it does have the option to hike again should inflation prove uncooperative, we are expecting it to hold rates at this level for most of 2023, before cutting at the end of the year to drive a better balance between interest rates being too far in restrictive territory and a weakening economy,” he added.

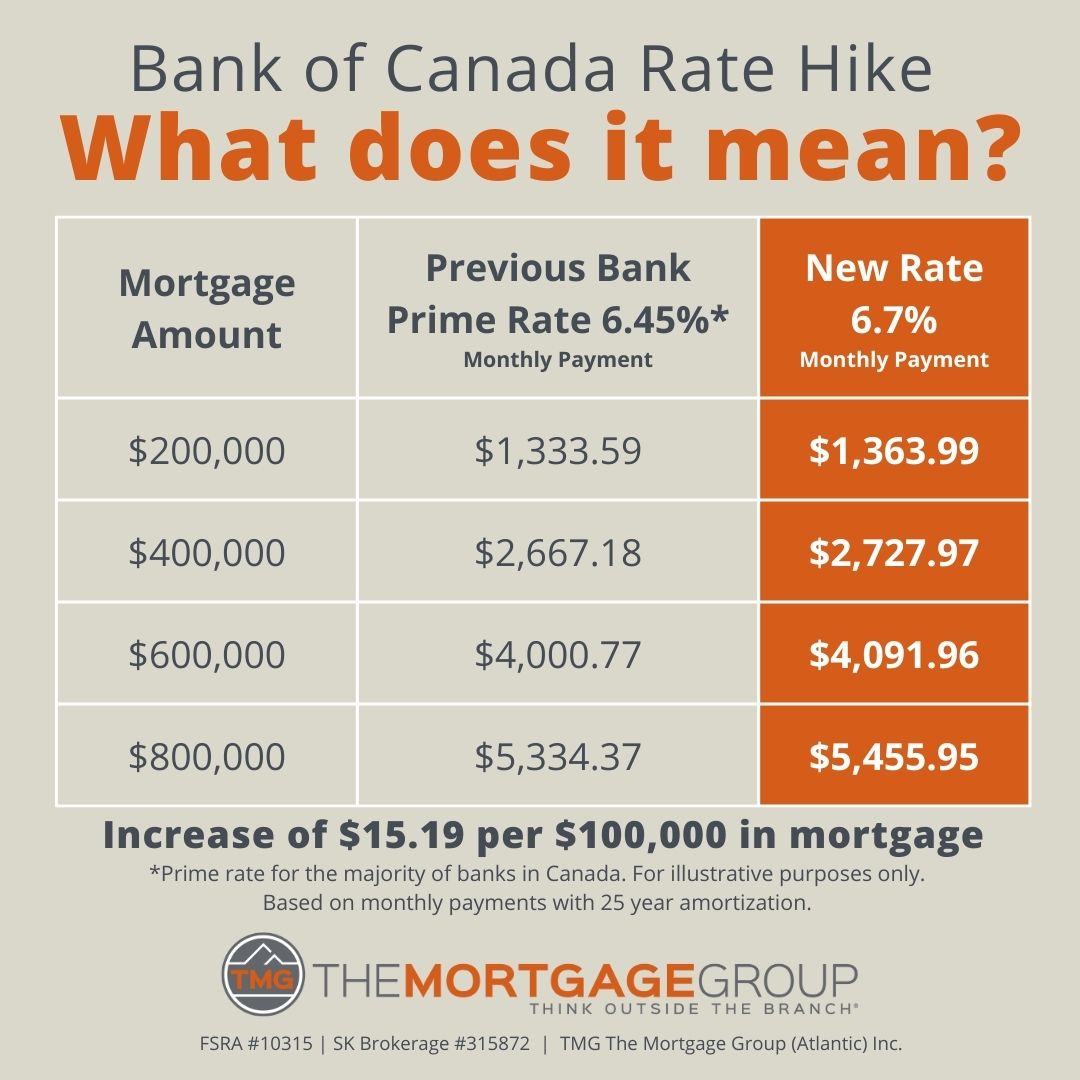

Prime rate climbs to 6.70%

Soon after the rate decision, the country’s largest banks announced increases to their prime rates, which will take effect on Thursday.

The prime rate at most financial institutions is now 6.70%, its highest level since 2001.

For variable-rate mortgage holders and those with a line of credit, this will translate into a monthly payment increase of nearly $16 per $100,000 of mortgage, based on a 30-year amortization.

The actual monthly payment will only vary for those with an adjustable-rate mortgage. However, most variable-rate mortgages come with fixed monthly payments. In those cases, the monthly payment will remain the same, but the portion going towards interest will increase while the portion going towards principal repayment will decline.

For those concerned about the sharp rise in interest costs over the past year, or facing a mortgage renewal in the coming months, a mortgage broker can go over all of the options that are available to you.

|